You’ve found your perfect Disney Vacation Club (DVC) resale contract, and you’re excited to make the “Welcome Home” moment official. For many buyers, financing is the strategic tool that makes joining DVC possible without liquidating investments.

But in the complex world of DVC loans, the numbers can be deceiving. A low monthly payment can seem ideal, but a slight change in terms can cost you thousands more over the life of your ownership. At Vacation Club Loans, we believe an educated buyer is a wealthier, we mean happier owner.

Our philosophy is to help you win on the facts by avoiding three common industry pitfalls that quietly erode your savings.

1. Eliminate Initial “Surprise Costs”

When you see the final closing disclosure, you will find a stack of necessary costs, from broker fees to mortgage recording fees. But many lenders add to this stack with an Origination Fee, often $200 or more, just to prepare the loan.

- The Difference: We are committed to keeping your initial “cash out-the-door” as low as possible. Vacation Club Loans eliminates this Origination Fee entirely, keeping that cash in your pocket. This transparency allows you to budget confidently from day one.

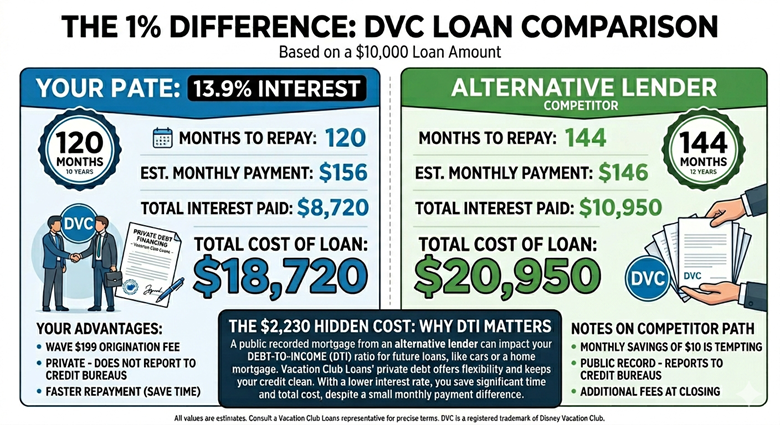

2. The Power of the 1% (Lower Interest)

Interest rates are a critical part of any long-term financial decision. Many lenders offer “convenience rates” that are simple to apply for but often carry a heavy interest rate higher than necessary.

- The Difference: We utilize sophisticated lending models to offer very competitive interest rates. While a 1% difference might only change your monthly bill by $15, over a typical 10-year loan, that 1% lower interest saves you thousands of dollars. We believe that your money belongs in your vacation budget, not your interest statement.

3. Two Years Closer to “Paid In Full”

The easiest way a lender can lower your monthly payment is to extend your loan term. While a standard 10-year term is optimal for equity, it is common in the industry to stretch loans to 12 or 15 years.

- The Difference: Our goal is to get you out of debt and into full, unrestricted ownership as efficiently as possible. Our focus on two years less of payments (getting you home by month 120 instead of 144) not only shaves thousands off the total interest paid but also lets you start enjoying your points without a monthly payment significantly faster.

Win on the Facts. Choose the Better Deal.

Joining DVC is a joyous event, and your financing should support that magic, not detract from it. At Vacation Club Loans, we don’t just provide funding; we provide a balanced, efficient path to membership.

Compare the real numbers on your dream contract and see how much you save. Use our instant [DVC Loan Calculator] to get the facts you need to make the smartest decision.